6 days Ago

6 days Ago

JLL identifies $1 trillion is needed to revitalize office spa ce at risk of obsolescence as part of shaping a more resilient built environment CHICAGO , Nov. 19, 2024 /PRNewswire/ -- The global commercial real estate market continues to rapidly evolve as shifting preferences for how space is used and where development takes place conflate with tightening sustainability requirements, strained national and local finances and infrastructure. JLL's (NYSE: JLL ) latest research " Opportunity through obsolescence, " is the first in a series of articles exploring the multifaceted opportunities found in assessing existing challenges in the built environment – including age and design, regulatory pressures and location – and turning them into value and returns.

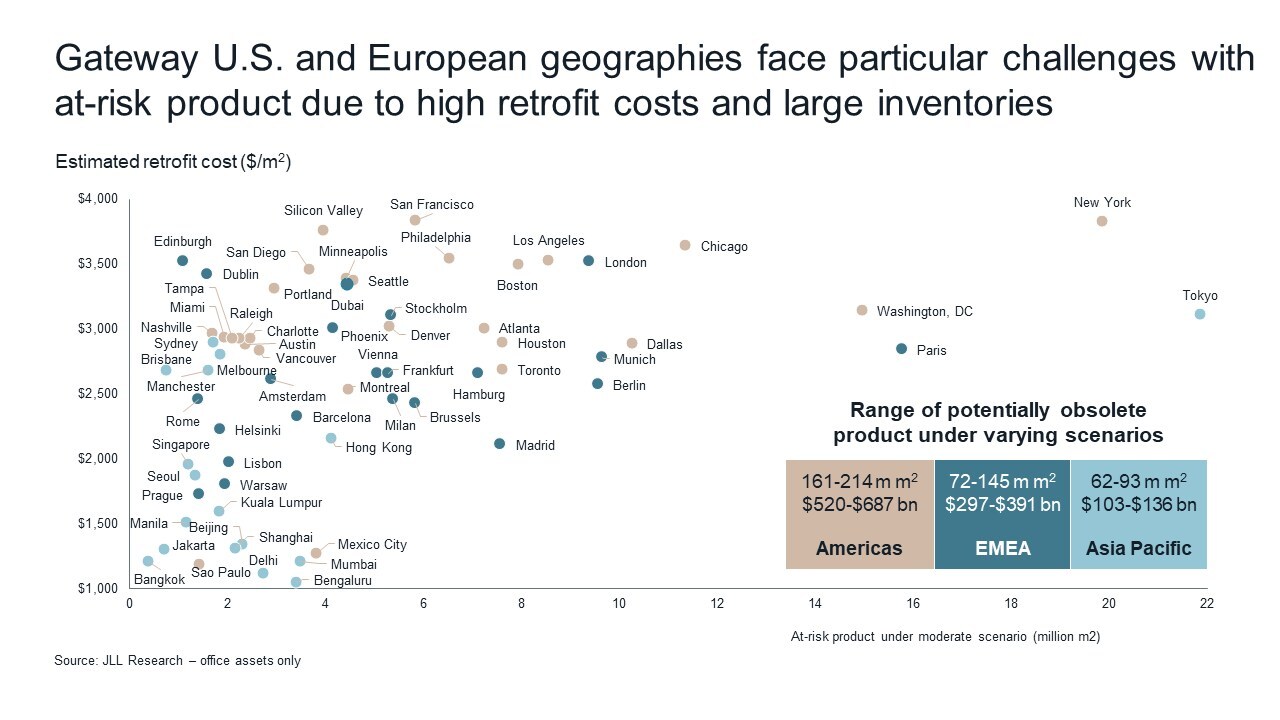

JLL finds that of the 776 million square meters of existing office space across 66 markets globally, about half of that space, or 322-425 million square meters, is likely to require substantial investment to remain viable in the near term – an investment of approximately $933 billion - $1.2 trillion in spending. Proactive engagement to retrofit and update existing assets will be key to unlocking opportunities for value creation through strategic investment and adaptation, particularly in the U.

S. and Europe , where 78% of office product and 83% of necessary capex is found. "The commercial real estate landscape is at a turning point as property owners and cities look to establish long-term viability of existing buildings and districts, in the face of evolving experiential and spatial preferences, increasing regulatory pressures , climate risk and changes in real estate demand," said Cynthia Kantor , CEO, Project & Development Services, at JLL.

"By proactively assessing and addressing outdated and at-risk buildings, owners can unlock significant value, create a more sustainable, resilient built environment and drive future returns." "The full potential of existing assets, both those nearing the end and earlier in their lifecycle, can only be realized through collaboration between stakeholders and by considering how various levels of obsolescence interact," said Phil Ryan , Research Director at JLL. "Owners and cities should assess how their portfolios holistically fit into their respective built environments and how a variety of factors contribute to their ability to respond to changing locational preferences and new sustainability and development regulations to create future value.

" Considering the risks and opportunities of building age and design Although there is no one measurement to calculate near-term stranding risk, building age tends to correlate best with the ability to meet tenant, investor and sustainability requirements along with the rate of occupancy and rent growth. In addition to significant capital needs, building age also contributes to an uneven distribution of capital investment required to keep at-risk buildings viable. Forty-four percent of projected obsolescence is likely to be in the U.

S. given higher levels of structural vacancy, along with an additional 34% in Europe , as flight to quality in select segments leads to a smaller but still significant amount of vacant product. This disconnect also exists in New York , Washington DC , Paris , Chicago and London , accounting for $242 to $320 billion of necessary global capital expenditures.

Meeting Sustainability and Regulatory Requirements The built environment accounts for up to 42% of global emissions annually, driving pressure from the public and private sector onto building owners to decarbonize properties. Even with the rate of building emissions beginning to flatline, to meet net-zero targets, the scale of retrofitting will need to accelerate to address the more than 86 million square meters of office product in need of near-term capex across the top eight markets for regulatory stranding risk due to tightening compliance standards alone. While sustainability requirements also incur upfront expenses, there is an impressive return on investment over an asset's lifecycle.

Whole-building retrofits involving a 40% to 65% energy use reduction have an average savings of $31 per square meter per year. If applied under a medium scenario for global at-risk office product in the eight highest-risk markets for stranding, this would yield $2.7 billion in annual energy savings alone for institutional office owners, all while tenant and investor demand for low-carbon buildings continues to increase.

Considering the geographic concentration of emissions, the rewards from decarbonization scale rapidly as well. For example, over 52 million square meters of current office assets across Boston , Washington DC , Paris , London , Seoul and Tokyo are likely at risk of functional obsolescence, but over 60% of emissions in these areas originate from the built environment, creating momentum to accelerate wholesale retrofitting and meet net-zero targets. Even with asset classes earlier in their life-cycle journeys, such as data centers, sustainable solutions will be important given the sectors' significantly higher site energy use intensity, as compared to other, potentially older asset classes.

Accounting for Locational Considerations Along with the asset- and regulation-driven stranding risks, is the growing demand for cohesive, amenitized and balanced spaces that are attractive to all potential stakeholders, from residents to workers and visitors. Local leaders and cities shifting focus to both high-level regeneration and smaller reparative approaches to reflect such spaces are already beginning to see the benefits. Strategies for repurposing and retrofitting buildings vary widely across markets, with U.

S. cities increasingly opting for large-scale conversion of office product to residential, hotel, lab and other uses. In Europe on the other hand, where structural vacancy is lower, targeted interventions for specific buildings can help to achieve overarching goals from city authorities to improve the public realm and enhance placemaking initiatives aimed at attracting workers back to office-heavy business districts and create inviting neighborhoods for visitors and residents.

About JLL For over 200 years, JLL (NYSE: JLL ), a leading global commercial real estate and investment management company, has helped clients buy, build, occupy, manage and invest in a variety of commercial, industrial, hotel, residential and retail properties. A Fortune 500 company with annual revenue of $20.8 billion and operations in over 80 countries around the world, our more than 111,000 employees bring the power of a global platform combined with local expertise.

Driven by our purpose to shape the future of real estate for a better world, we help our clients, people and communities SEE A BRIGHTER WAY SM . JLL is the brand name, and a registered trademark, of Jones Lang LaSalle Incorporated. For further information, visit jll.

com. Contact: Allison Heraty Phone: 1 312 228 3128 Email: [email protected] SOURCE JLL.