Jetstar passengers left stranded, unable to check into flights after airline confirms nationwide tech outage

Passengers flying on a major Aussie airline have been left stranded at the terminal following a major technical outage....

Passengers flying on a major Aussie airline have been left stranded at the terminal following a major technical outage....

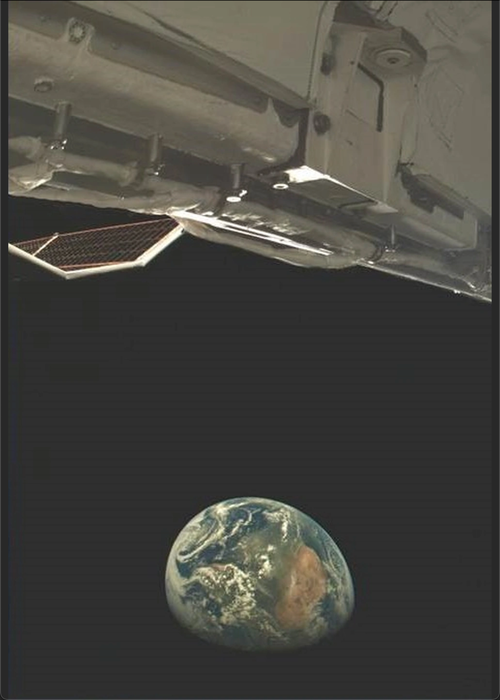

First In-Orbit Image Released From Classified X-37 Spaceplane On Thursday evening, the Secretary of the Air Force Public...

Ignoring 1 letter could see pensioners missing out on back payments worth nearly £8,000...

Stocks to buy or sell: Experts recommend four shares under ₹100 — SJVN, IDFC First Bank, ZEEL, and International Con...

A first home buyer has pounced on a Stanmore property for just $852k and he’s grateful for a rate cut and some help fr...

Reiterates recommendation for slashing of authorisation (license) fee to 3 per cent of AGR from 8 per cent...

In India, gold prices surged by Rs 9,506 in seven weeks to Rs 86,020 per 10 grams on the MCX, compared with Rs 76,544 re...

KUALA LUMPUR: Autocount Dotcom Bhd (ADB), through its wholly-owned subsidiary Auto Count Sdn Bhd, launched AutoCount One...

KARACHI - The State Bank of Pakistan (BPS) injected Rs1,754 billion in the market through reverse repo purchase and Shar...

We need to relook and reform the state entertainment tax on cinema; the burden of double taxation is a growing concern, ...

Mapping The Growth Of Government Submitted by OpenTheBooksAs DOGE continues searching for and flagging waste, fraud and ...

EPFO: Now EPFO subscribers will be able to withdraw PF money directly through UPI. This will make the claim proces...

From US and Russia holding talks on Ukraine war to Tesla signalling India entry plans, here are the key talking points t...

The Uttar Pradesh police's SIT has filed a 4,000-page chargesheet in six of the 12 cases related to the November 24 Samb...

In addition to the Q3FY25 GDP data, the government will also release the second advance estimate for the full-year GDP o...

Since the start of this flu season, Ohio has seen more than 9,000 flu hospitalizations. Hamilton County has had the seco...

Glacier Media has announced the upcoming closure of three Metro Vancouver community news websites. A statement posted on...

ALP Heating, a Vaughan-based company secures its second consecutive ‘Best of the Best’ award and third ‘Best of Aw...

Uncertainty in the federal government has caused investors to be cautious about this REIT....

Buy or sell: Sumeet Bagadia recommends three stocks to buy on Monday — IndiGo, Coal India, and Larsen and Toubro (LT)...

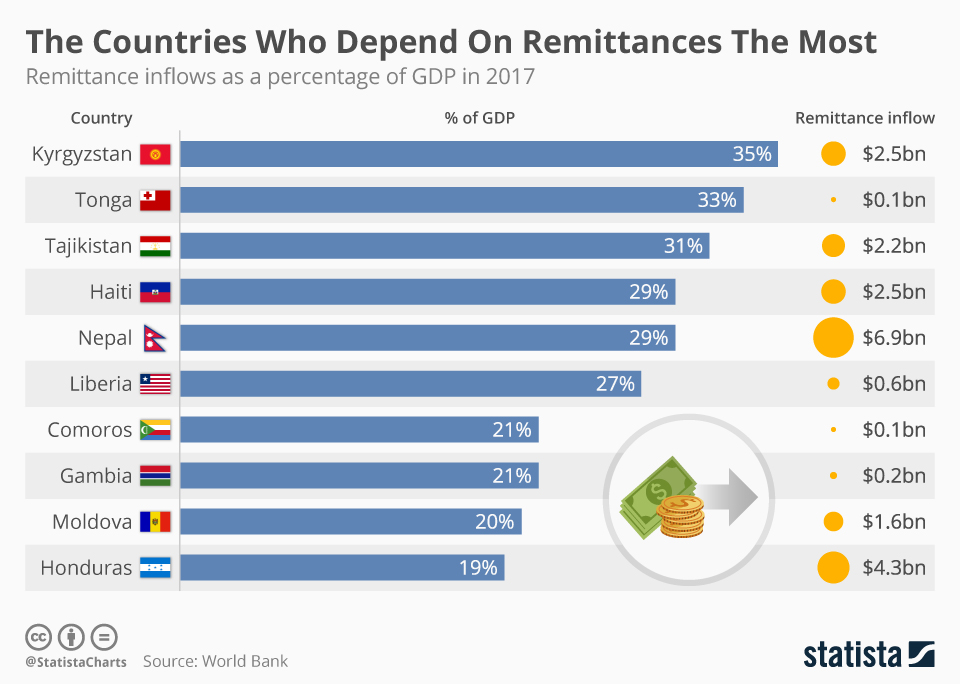

These Are The Countries Who Depend On Remittances The Most Remittance inflows to low- and middle-income countries rose t...

Economic pressures and a desire for enhanced personal wellbeing are driving a shift in the Filipino workforce. Employees...

The charges are imposed on bill payments such as electricity and gas bills made using the platform. The fee ranges from ...

With consumers increasingly seeking convenience, transparency, and personalised experiences, D2C brands have emerged as ...

GaadiWaadi -The final production-spec version of the highly anticipated BMW F 450 GS ADV is slated for a global debut by...

LONDON, Feb 22 — A Hong Kong company has submitted an initial £7 billion (RM39.1 billion) bid for a majority stake in...

_0.jpg?itok=kFoyc4Pi)

Former CNBC Analyst To Admit Conning Investors Out Of Nearly $3 Million Authored by Jill McLaughlin via The Epoch Times ...

A spokesperson for Delta said it was declining to comment on pending litigation...

MARLBOROUGH, Mass., Feb. 21, 2025 /PRNewswire/ -- Boston Scientific Corporation (the "Company") (NYSE: BSX) today announ...

KUALA LUMPUR: The ringgit is expected to move towards its immediate support level of RM4.36 against the US dollar in the...

How to update new mobile number in Aadhaar: The process of changing the mobile number in Aadhaar card is not completely ...

Sales of previously occupied U.S. homes fell in January as rising mortgage rates and prices put off many would-be homebu...