New Renault Duster & 7-Seater Bigster To Likely Get Strong Hybrid Engine

GaadiWaadi -Renault’s electrified line-up in India will initially include two electric cars and likely even at least t...

GaadiWaadi -Renault’s electrified line-up in India will initially include two electric cars and likely even at least t...

...

...

Buy or sell: Sumeet Bagadia recommends three stocks to buy on Monday — Grasim Industries, TCS, and HUL...

From health trends to wellness strategies and medical discoveries, the world of health and wellness is so dynamic that i...

In an era where Google understands symptoms, digital marketing for dentists becomes non-negotiable. With almost 3 in 4 p...

ISLAMABAD - The Central Development Working Party (CDWP) has approved seven development projects with a cumulative cost ...

OXNARD, California, April 25, 2025 (GLOBE NEWSWIRE) -- Mission Produce, Inc. (NASDAQ: AVO) (“Mission” o "la Empresa�...

Q4 Results Today live updates 26th April 2025: Find all the latest Q4 results 2025 updates for India Cements, IDFC First...

ISLAMABAD - International Packaging Films Limited (IPAK) Group has recorded 66 percent increase in its revenues for the ...

At the same time, rural women are increasingly taking up jobs in agriculture, indicating a shift in employment patterns ...

ISLAMABAD - The Securities and Exchange Commission of Pakistan (SECP) has announced the establishment of a dedicated Lic...

On April 26, 2025, petrol and diesel prices in New Delhi, India, are Rs 94.72 and Rs 87.62 per liter. Prices vary by cit...

All Quiet On The Western Ports... Is This The Calm Before The Trade War Storm? All is quiet on the American front as the...

Malaysia's initial meeting with US officials on tariffs went well but it's only the first step toward forging a trade ag...

As lower crude prices are expected to ease inflationary pressure, support domestic growth, despite intensifying global t...

Notifies rules for GST appellate tribunals; provides for mandatory e-filing, hybrid hearing...

Carries search at company’s offices in Delhi, Gurugram and Ahmedabad...

Domestic household debt lower than other economies: Morgan Stanley...

Due to selling in Axis Bank, growing tensions along Indo-Pak border following terror attack at Pahalgam in J Mcap on BSE...

The global ratings agency believes the acquisition will support APSEZ’s efforts toward international diversification, ...

WASHINGTON, April 26 — US Treasury Secretary Scott Bessent urged Asian Development Bank President Masato Kanda to take...

KUALA LUMPUR, April 26 — The ringgit is expected to hover within a tight range of RM4.37 to RM4.38 next week, as marke...

MONTREAL — The Globe and Mail and the Toronto Star were the big winners as the National Newspaper Awards were handed o...

Today, we’re going to take a trip through the Stargate, a really cool plot device in a fictional universe now owned by...

The following Slate pickup truck video is about one of the more intriguing and exciting recent EV developments. With inc...

Craig McRae confirms a key Magpie will miss up to eight weeks with a knee injury, as the Saints look upset the Lions at ...

Recent Decentraland (MANA) price analysis points to a potential recovery as the token rebounds by more than 70% from its...

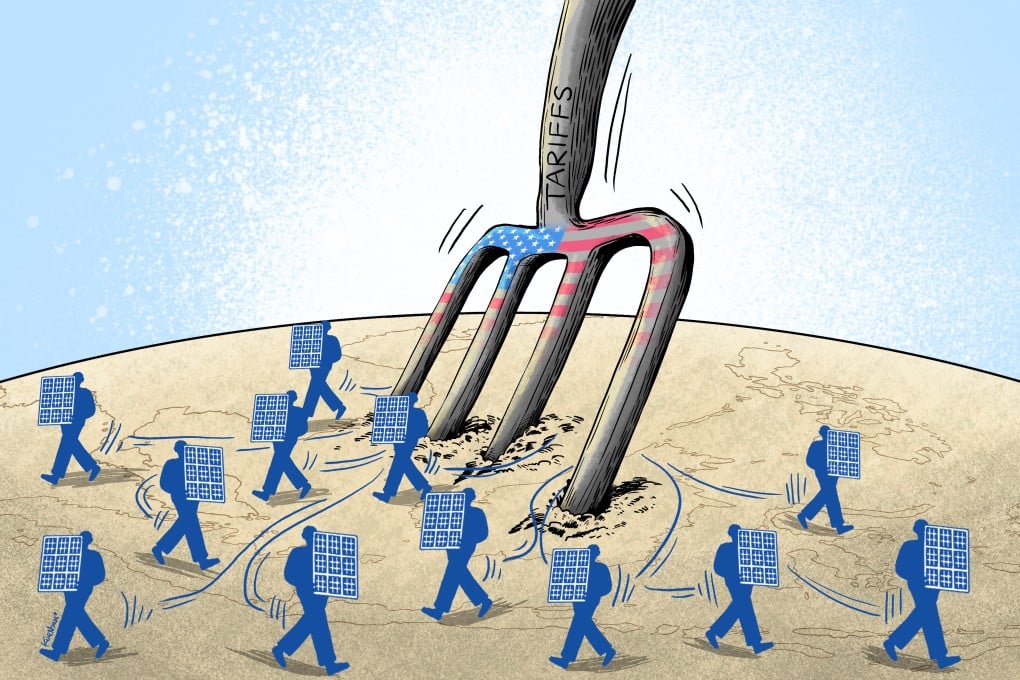

Chinese firms have been exporting from offshore factories to beat US tariffs for a decade, and Washington is determined ...

The National Social Security Fund (NSSF)on Friday, kicked off its 60th anniversary celebrations with its Annual General ...

High Court orders Energy Ministry to make public approved projects in the county after failure to comply with a similar ...

Stakeholders in the financial sector have cited a lack of political will as one of the major barriers to achieving finan...

Despite cracks in the walls and its dilapidated state, a house in Melbourne’s inner north has scored an almost-$1m sal...

The company, with significant market shares in passenger and commercial vehicles, is set to benefit from the rise of ele...

NEW YORK and NEW ORLEANS, April 25, 2025 /PRNewswire/ -- Kahn Swick & Foti, LLC ("KSF") and KSF partner, former Attorney...

NEW YORK and NEW ORLEANS, April 25, 2025 /PRNewswire/ -- Kahn Swick & Foti, LLC ("KSF") and KSF partner, former Attorney...

NEW YORK and NEW ORLEANS, April 25, 2025 /PRNewswire/ -- Kahn Swick & Foti, LLC ("KSF") and KSF partner, former Attorney...

NEW YORK and NEW ORLEANS, April 25, 2025 /PRNewswire/ -- Kahn Swick & Foti, LLC ("KSF") and KSF partner, former Attorney...

The New Orleans Saints added an athletic safety with the No. 93 overall pick in Virginia's Jonas Sanker....