5 hours Ago

5 hours Ago

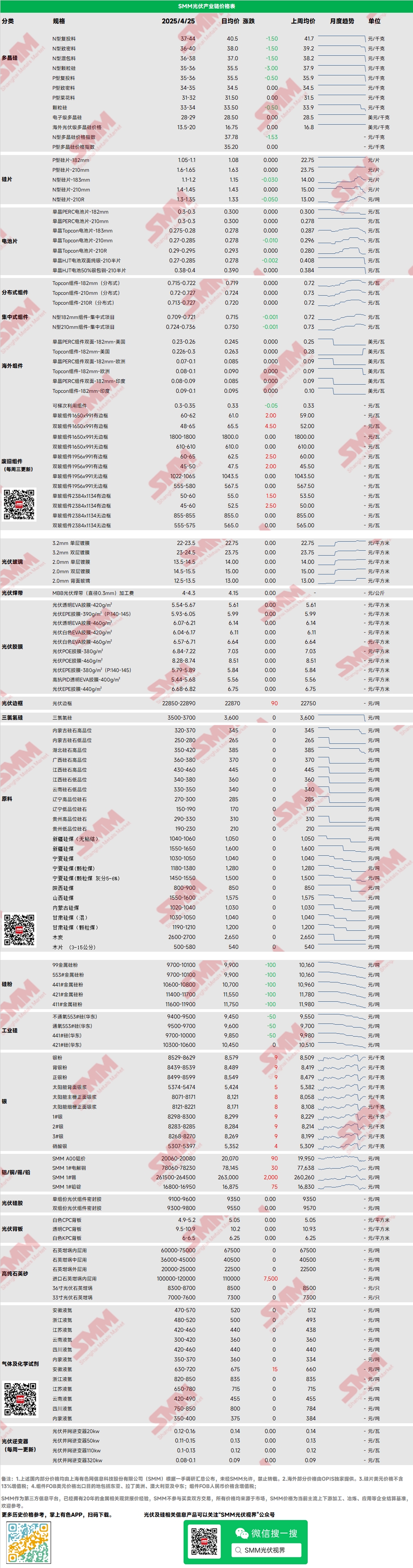

Polysilicon: This week, the mainstream transaction prices for N-type recharging polysilicon were 37-44 yuan/kg, and for N-type dense polysilicon, 36-40 yuan/kg. Polysilicon prices continued to decline, with some companies' transaction prices falling below the current mainstream quotations. The spot market for polysilicon showed a clear downward trend.

An industry meeting was held on Wednesday, and the resumption of production by some polysilicon companies will be discussed in subsequent meetings. Some companies may have production cut plans in May. Companies are beginning to intentionally maintain the current market, but it is important to note that downstream sentiment has not improved, and polysilicon inventory is under pressure.

Downstream companies are currently in a price-driving mindset. Wafer: This week, domestic N-type 18Xmm wafers were priced at 1.1-1.

2 yuan/piece, N-type 210R at 1.3-1.35 yuan/piece, and N-type 210mm wafers at 1.

4-1.45 yuan/piece. Wafer prices continued to pull back, with a decline across all sizes.

Wafer companies held an industry meeting on Tuesday, adjusting Q2 quotas downward. Expectations for subsequent wafer and cell production cuts are high, which may help alleviate the supply surplus. Cell: This week, solar cell prices continued to decline, with no bottom in sight, and the overall outlook remains bearish.

The 183 cells saw a sharp drop, with the lowest quotation plummeting from 0.28 to 0.27, which is expected to become the mainstream quotation in the short term, mainly due to the surplus supply of 183.

The 210r is expected to continue falling, from 0.28 to 0.275 in the near term.

The 210N cell prices remained relatively firm, with mainstream prices at 0.295-0.30 yuan/W.

This week, solar cell demand and cost support continued to weaken, market trading volume declined, and related companies have expectations for production cuts. Module: This week, the decline in module prices narrowed. Distributed N-type 182 modules are currently priced around 0.

715-0.722 yuan/W, with the average price down by 0.007 yuan/W WoW.

Distributed N-type 210 modules are currently priced at 0.72-0.727 yuan/W, with the average price down by 0.

007 yuan/W WoW. Distributed N-type 210R modules are currently priced at 0.713-0.

727 yuan/W, with the average price down by 0.009 yuan/W WoW. Centralized N-type 182 modules are currently priced at 0.

709-0.721 yuan/W, with the average price down by 0.009 yuan/W WoW.

Centralized N-type 210 modules are currently priced at 0.724-0.736 yuan/W, with the average price down by 0.

011 yuan/W WoW. This week, the decline in module prices narrowed. The spot sales price including tax in April remained above 0.

7 yuan/W, but the forward order price including tax for May delivery has fallen below 0.65 yuan/W, with an accelerated downward trend. The above situation indicates that before the 5.

31 period, domestic supporting policies lack continuity, and companies are relatively pessimistic about the future market, with a significant reduction in forward module orders. In addition, with the continuous decline in main material prices and the rise in auxiliary materials such as silver glass, integrated module companies are further burdened by non-silicon cost increases, and the proportion of subsequent production cuts is expected to increase significantly. Terminal: From April 14 to April 20, 2025, SMM statistics showed that domestic companies, including LONGi Green Energy Technology Co.

, Ltd., Jinko Solar Co., Ltd.

, and JA Solar Technology Co., Ltd., won a total of 37 PV module project sections, of which 18 disclosed installed capacity.

This week, the procurement of finalized module models included N-type and P-type PV modules. The winning bid price distribution for modules was concentrated at 0.69-0.

95 yuan/W; the weekly weighted average price was 0.72 yuan/W, down by 0.01 yuan/W WoW; the total procurement capacity was 742.

50 MW, a decrease of 209.77 MW WoW. The N-type module procurement capacity for the week was approximately 462.

53 MW, accounting for 62.29%. EVA: This week, the settlement price for PV-grade EVA remained at 11,550-11,950 yuan/mt, with a slowdown in transaction pace and a strong market wait-and-see sentiment, showing a volatile trend.

Foam-grade and cable-grade EVA fell by 100 yuan/mt WoW. On the supply side, some petrochemical companies shifted production to PV-grade EVA, and spot supply gradually recovered. On the demand side, the installation rush is nearing its end, and with the expected decline in new film orders in May, supply recovery and demand contraction are expected to lead to a downward trend in EVA prices.

Film: The mainstream price range for EVA film was 13,300-13,500 yuan/mt, and for EPE film, 15,200-15,500 yuan/mt, with prices remaining stable. On the demand side, module prices showed a downward trend, and the installation rush is nearing its end, with demand gradually slowing. It is expected that new film order prices in May will show a downward trend, and the cost-side PV-grade EVA prices are expected to decline, providing cost support for the downward trend in film prices.

POE: Domestic delivery-to-factory prices for POE remained stable at 12,000-14,000 yuan/mt, with prices temporarily steady. Although some petrochemical plants are undergoing maintenance, under the dual impact of weakening installation demand and new capacity release, PV-grade POE prices are expected to be under pressure and decline. PV Glass: This week, some PV glass companies slightly raised their quotations.

As of now, the mainstream quotation for domestic 2.0mm single-layer coating is 14.0 yuan/m2, with a mainstream transaction price of 13.

7 yuan/m2. The mainstream quotation for 3.2mm single-layer coating is 22.

5 yuan/m2, and for 2.0mm back glass, 13.0 yuan/m2.

This week, some PV glass companies slightly raised their quotations by 0.5 yuan/m2, but high-price order acceptance was poor. Module companies, against the backdrop of their own price declines, remain strongly resistant to rising raw material prices.

In the near term, upstream and downstream companies are expected to be in a stalemate, but with the decline in module production schedules, high prices are expected to be difficult to transact. High-Purity Quartz Sand: This week, domestic leading high-purity quartz sand companies continued to raise their mid-layer sand quotations, while other sand prices remained stable. Current market quotations are as follows: inner-layer sand at 65,000-75,000 yuan/mt, mid-layer sand at 36,000-45,000 yuan/mt, and outer-layer sand at 20,000-25,000 yuan/mt.

This week, domestic leading quartz sand companies slightly raised their mid-layer sand quotations, but downstream crucible companies have not yet accepted the price increases, mostly adopting a wait-and-see attitude. With the expected narrowing of trade war tariffs, import sand prices may slightly decline, and market panic sentiment has slightly eased. It is expected that the transaction center for quartz sand will slightly pull back.

View SMM PV Industry Chain Database.