2 weeks Ago By [email protected] (Ryan Vanzo)

2 weeks Ago By [email protected] (Ryan Vanzo)

Looking for profitable energy stocks? Check out what Warren Buffett owns. He's been a major energy investor for decades, investing in a wide range of verticals, everything from upstream and refining to large scale renewable projects. Currently, the fifth-largest position in his publicly traded portfolio is an energy company everyone has heard of -- and there's a great investment case to be made for it right now.

Secure a reliable 5%-plus shareholder yield After a brief correction, now looks like a great time to buy Chevron ( CVX 2.46% ) stock. The dividend yield is currently around 4.

4%. But when you add in the company's massive share repurchases -- the company is authorized to buy back up to $75 billion in stock -- the total shareholder yield surpasses 5%. Warren Buffett is clearly a big fan of Chevron's capital allocation strategy.

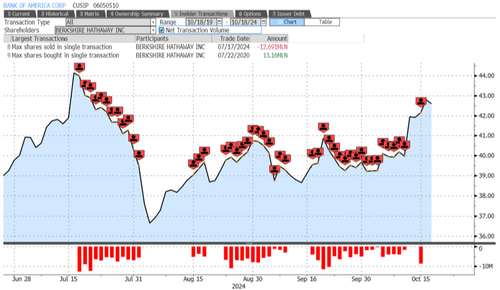

His holding company, Berkshire Hathaway , owns 118 million shares worth a hefty $18.5 billion -- roughly 6.4% of Chevron's total value.

Berkshire has been a net seller of late, but that's likely due to a massive investment in another oil and gas company: Occidental Petroleum . It's likely Buffett simply doesn't want to overexpose his portfolio to a single sector. But he's clearly still an oil bull -- two of his top six positions are now oil and gas companies .

Over the last two decades, Chevron's integrated approach has resulted in an impressive financial performance. Its return on invested capital , or ROIC, a measurement of how effectively it uses capital to generate profits, have averaged above 10% over that time period. And healthy free cash flow has allowed it to support a sizable dividend all while consistently reducing its share count.

In spite of this, the company currently trades at a respectable free-cash-flow yield of 6.6% -- well above its long-term average. CVX Free Cash Flow Yield data by YCharts Chevron had been beating the S&P 500 over the past two decades until the recent correction in oil prices.

Over the past 12 months, oil prices have fallen from $90 per barrel to around $70 -- the direct cause of Chevron's declining share price. But if you're bullish on oil prices from here, now could be a great time to initiate a position. CVX Total Return Level data by YCharts If you're bullish on oil, Chevron stock is a no-brainer Even though Chevron has exposure to both midstream and downstream assets -- which provides it some insulation from oil price volatility -- it still makes most of its money from upstream operations.

That means that long-term, you must be bullish on oil prices to justify an investment in Chevron. Even if oil prices remain flat, there's still an investment case to be made for Chevron. That's because it has been able to economically replace its reserves and drive enough operating efficiencies to meaningfully improve its profits per barrel, even without the help of rising oil prices.

From 2015 to 2019, for instance, oil prices averaged just under $60 per barrel. Over this time period, Chevron generated profits per barrel of around $7. Over the next few years, however, management expects to produce profits between $10 and $11 per barrel.

And that's assuming oil prices are in the low $60s -- over 10% down from current levels. These rosy profit estimates come even as Chevron pushes to expand production by around 20% by 2027. If you're bullish on oil, investing in Chevron is a no-brainer.

Over the next few years, production should rise, as should profitability, all while the company returns billions of dollars to shareholders through dividends and stock repurchases. And with a challenging geopolitical climate, there's upside to rising oil prices as well, while mitigating downside risk given Chevron's diversified midstream and downstream assets, which can generate positive cash flows even if market conditions temporarily turn sour..